Retirement under the Federal Employee Retirement System doesn’t affect government workers alone. If you’re a federal employee, you’ve probably also been choosing and arranging your coverage to provide for your family under FERS as well.

No one wants to imagine what life might be like for their loved ones if they were to pass on first. But if that happened…do you know what you would be leaving with your family?

THE THREE SURVIVOR ANNUITY PLANS AVAILABLE FOR FERS RETIREES

Under the federal retirement system, you have three Survivor Annuity Plans available:

- The 50% Benefit

- The 25% Benefit

- No Spousal Benefit (default)

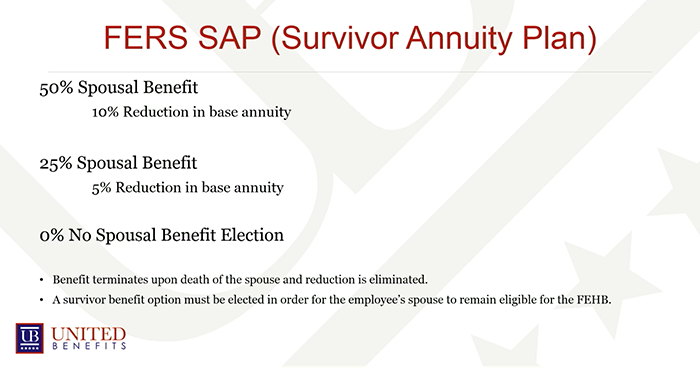

THE 50% BENEFIT SURVIVOR ANNUITY PLAN

Of the three plans, the 50% spousal benefit is the most robust. If you were to pass away before your spouse, they would continue to receive half of your FERS annuity for the rest of their lifetime. To offset that cost, however, your pension will be reduced by 10% while you’re still living.

THE 25% BENEFIT SURVIVOR ANNUITY PLAN

Your second option is to select the 25% spousal benefit, which would reduce your retirement by 5% while you’re still living. This Survivor Annuity Plan would provide your spouse with a quarter of your regular annuity if you were to pass away before them.

THE NO-BENEFIT SURVIVOR ANNUITY PLAN

The third option you have is the default plan every federal worker begins with (since not everyone is married). This option leaves no spousal benefit, and you keep your full pension within your lifetime.

If you want to leave some sort of spousal benefit from your FERS annuity, then you need to opt in for one of the other plans.

WHAT ARE THE PROS AND CONS OF THE SURVIVOR ANNUITY PLANS?

One of the major factors of choosing a Survivor Annuity Plan is the overall cost involved: both during your retirement, and after either you or your spouse pass away.

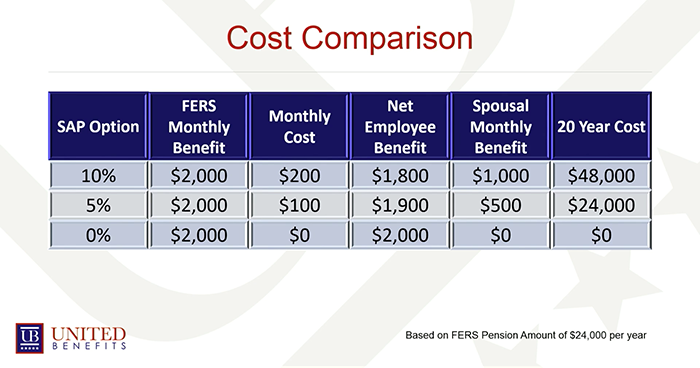

Let’s say, for example, your FERS annuity pays you $24,000 a year (or $2,000 a month).

If you chose the maximum Survivor Annuity Plan for your spouse, that would reduce your retirement by 10% ($200), so your retirement now would be $1,800 a month.

If you were to pass away before your spouse, your spouse would receive $1,000 a month: 50% of your total FERS annuity. However, if you look at the cost of that plan over a 20-year period, that’s going to cost your retirement $48,000.

The Survivor Annuity Plan, in essence, reduces your retirement to insure your life. The problem is, is if your spouse passes away before you do, then that money is wasted. There’s not another beneficiary that’s going to receive anything from it.

So instead, some federal employees do what’s called a pension maximization strategy.

A PENSION MAXIMIZATION STRATEGY

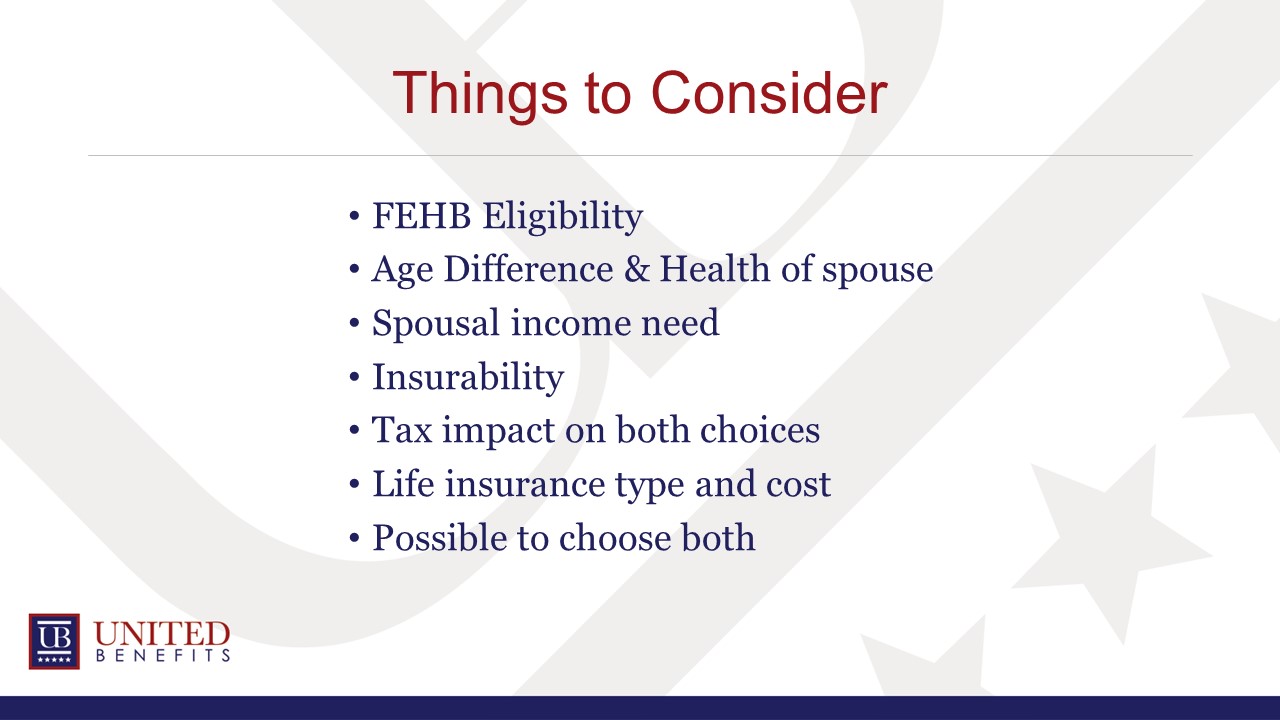

Instead of cutting down on your retirement pension, you can actually insure yourself with life insurance for your spouse. If Pension Maximization is something you might be interested in, then you need to keep your FEHB (Federal Employee Health Insurance) in mind.

If your spouse needs to maintain your health insurance, then you will need to leave your spouse part of your FERS annuity for them to be eligible to continue FEHB in the event of your passing. To determine if pension maximization is the right decision for you, you also need to think about your age, your spouse’s age, your health, your spouse’s health, and the way your FERS is taxed versus the way life insurance is taxed.

It’s also possible to (and a lot of federal employees do) choose both. Instead of doing the 50% plan with the 10% reduction, they choose the 5% reduction; leave their spouse 25%; and put in a life insurance policy that can benefit their entire family. So, there’s a lot of different things to consider.

IF SOMETHING HAPPENED TO YOU, WOULD YOUR LOVED ONES BE PROVIDED FOR?

United Benefits has assisted thousands of federal employees on several impactful topics. We can help you, too. Ask us anything!

Click here to request a consultation and talk one-on-one with a representative about the options available to you.